Press Release No. 19/265

3 July 2019

On 12 June 2019, Executive Board of the International Monetary Fund (IMF) concluded the Article IV consultation with Grenada.

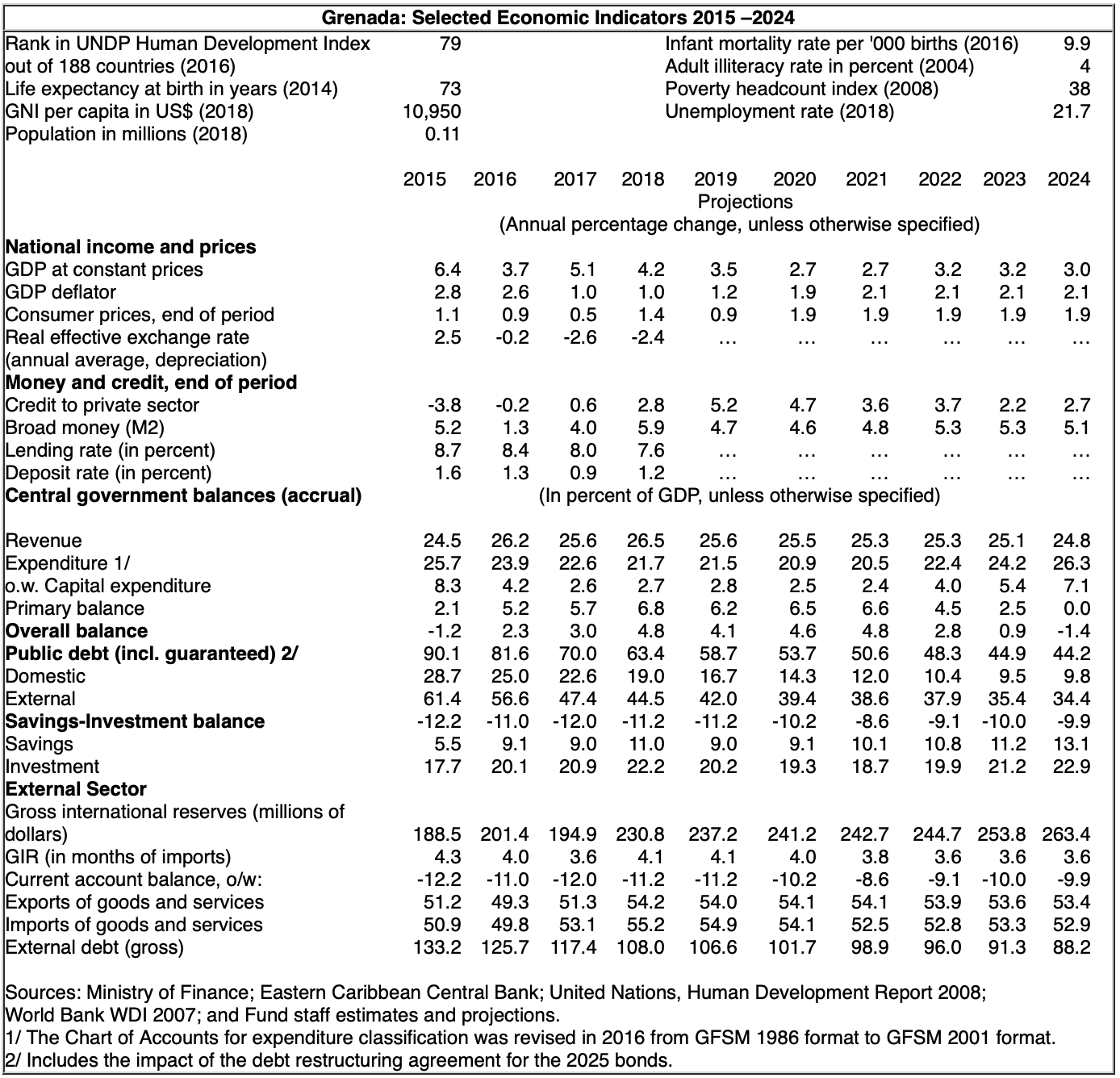

The Grenadian economy continues to grow robustly. GDP expanded by 4¼% in 2018, driven by strong activity in construction and tourism. Unemployment has been falling, but it remains high at 21.7% as of mid-2018. Inflation has remained low and bank credit growth is positive. The external current account deficit is estimated to have narrowed in 2018 due to strong tourism receipts, but it remains elevated at around 11% of GDP. Robust FDI flows, including from the citizenship-by-investment (CBI) programme, are financing the external deficit while supporting economic growth.

Adherence to the fiscal responsibility law (FRL) has enabled further debt reduction. The fiscal surplus increased further in 2018, reflecting a combination of strong revenues and the FRL-mandated expenditure restraint. Low execution of grant financing and institutional bottlenecks in project execution combined to keep capital outlays subdued at 2¾% of GDP. Central government debt fell from 70 to 63½% of GDP in 2018, but arrears to Algeria, Libya, and Trinidad and Tobago remain to be regularised.

Growth is set to remain above potential in 2019, but is projected to ease somewhat over the medium-term, consistent with a waning of FDI-driven construction. The fiscal position is projected to loosen over the medium term in line with the FRL’s provisions that take effect after public debt falls below 55% of GDP and should provide some support to the economy. External risks are mainly on the downside and are centered on prospects for U.S. growth and global financial conditions. Domestic risks are two-way and partly hinge on the efficiency of the envisioned fiscal expansion that is permitted by the FRL.

Executive Board Assessment

Executive Directors welcomed Grenada’s continued strong economic and fiscal performance and sustained debt reduction, underpinned by sound policies. They emphasised that further policy improvements and public support for reforms are critical to achieve higher and broad-based medium-term growth, further reduce unemployment, entrench debt sustainability, and strengthen financial stability.

Directors underscored the importance of focusing policy efforts on making growth more resilient, sustainable, and inclusive. They noted that Grenada’s growth potential is held back by susceptibility to economic shocks and natural disasters in addition to long-standing structural weaknesses such as high unemployment and an external competitiveness gap. In this context, directors supported making prudent and efficient use of Grenada’s hard-earned fiscal space to address the country’s infrastructure and resilience gaps. They highlighted the need to enhance the business climate and competitiveness, including through improvements in labour market institutions. They noted that education and training programmes to match job opportunities with the labour force are also needed.

Directors commended the authorities’ steadfast compliance with the Fiscal Responsibility Law (FRL). They agreed that the FRL could be enhanced, with a consistent and well-sequenced implementation, to facilitate more productive spending while safeguarding debt sustainability. In particular, they emphasised the need to improve the procedures for expenditure planning and classification. Directors welcomed the authorities’ intention to implement initiatives on pension reform and healthcare coverage in a manner that is consistent with the FRL and fiscal sustainability.

Directors encouraged the authorities to move ahead with fiscal structural reforms to improve spending quality and mitigate fiscal risks. They stressed the importance of implementing the public-sector management reform strategy to improve public sector productivity and service delivery. They recommended further strengthening social assistance programmes and continuing public investment management and public enterprise reforms, while regularising bilateral arrears. Directors welcomed the climate change policy assessment and the authorities’ intention to elaborate a comprehensive disaster resilience strategy with inputs from key stakeholders. This should help catalyse concessional financing to address the infrastructure and resilience gaps.

Directors welcomed steady improvements in bank credit growth and banking soundness indicators. At the same time, they noted that the continued fast growth in lending by credit unions and the rising property markets warrant close monitoring. They called for a proactive approach to strengthening the supervision and regulation of the non-bank financial sector by the local regulator and the need for coordination with the ECCB and the ECCU’s peer regulators. Directors highlighted the importance of continued efforts to ensure compliance with AML/CFT regulations in all areas to support correspondent banking relationships and preempt any financial integrity concerns.

[1] Under Article IV of the IMF’s Articles of Agreement, the IMF holds bilateral discussions with members, usually every year. A staff team visits the country, collects economic and financial information, and discusses with officials the country’s economic developments and policies. On return to headquarters, the staff prepares a report, which forms the basis for discussion by the Executive Board.

[2] At the conclusion of the discussion, the Managing Director, as Chairman of the Board, summarises the views of Executive Directors, and this summary is transmitted to the country’s authorities. An explanation of any qualifiers used in summings up can be found here: http://www.imf.org/external/np/sec/misc/qualifiers.htm